I. Introduction: The New Standard in Real Estate

In a world where we can buy a car from a phone, apply for a mortgage from a couch, and execute a $10 million business contract via DocuSign, why are we still tethered to physical desks for the final step of a real estate closing?

The answer, until recently, was the notary. The legal requirement for a commissioned notary public to physically witness a signature was the last analog bottleneck in an increasingly digital transaction chain. That bottleneck is now gone.

The SECURE Notarization Act, combined with Florida's comprehensive RON statute (Florida Statutes §117.201–§117.265), has ushered in a new era for the real estate industry. Remote Online Notarization is no longer a pandemic-era workaround — it is the preferred method for the modern consumer, and the competitive advantage for the Realtors and Title Officers who have mastered it.

This guide is designed for real estate professionals who want to understand the technology, leverage it for their clients, and eliminate the scheduling conflicts and re-draw costs that are quietly eroding their margins.

II. What Exactly Is Remote Online Notarization (RON)?

Before diving into strategy, it is worth establishing a precise definition — because the terminology is frequently confused.

Electronic Notarization (eNotarization) is an in-person notarization where the notary uses an electronic seal and the signer uses an electronic signature. The notary and signer are physically in the same room. This is not RON.

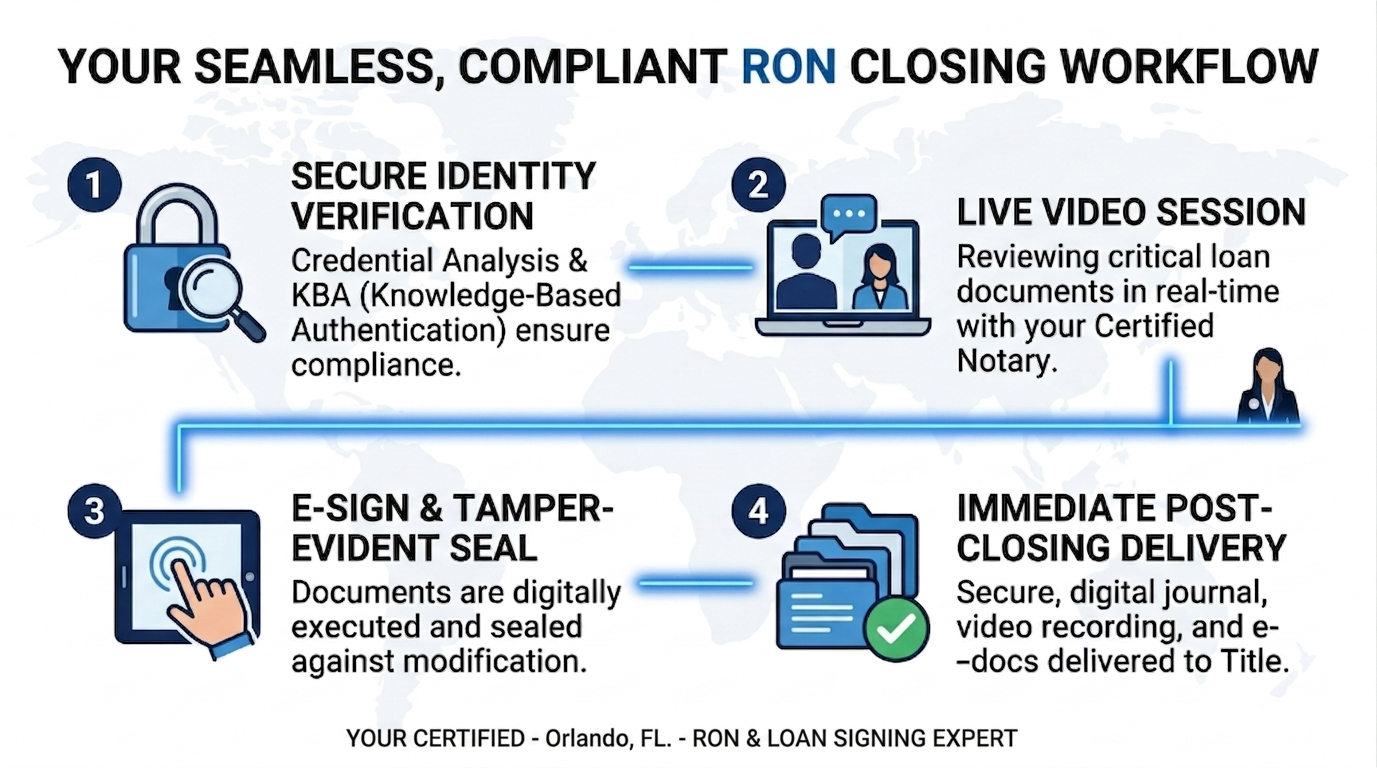

Remote Online Notarization (RON) is a notarization conducted entirely via a secure, real-time audio-visual connection. The notary and signer are in different physical locations. The signer's identity is verified through two layers of electronic authentication, and the entire session is recorded and stored as a permanent audit trail.

### The Two-Layer Identity Verification System

Florida RON law requires a more rigorous identity verification process than a traditional in-person notarization, where the notary relies solely on visual inspection of an ID.

Layer 1: Credential Analysis. The signer presents a government-issued photo ID to the camera. The RON platform's AI analyzes the ID in real time, checking for authenticity markers, verifying the format against the issuing state's standards, and confirming the ID has not expired.

Layer 2: Knowledge-Based Authentication (KBA). The signer answers a short quiz of five multiple-choice questions generated from their U.S. public records — previous addresses, vehicles owned, relatives' names. They must answer four out of five correctly within two minutes.

This two-layer system creates a stronger proof of identity than a traditional in-person notarization. A stolen ID alone is not sufficient to pass the KBA quiz.

### The Digital Vault: A Superior Audit Trail

Every Florida RON session is recorded in its entirety — audio and video — and stored in an encrypted digital journal for a minimum of ten years under Florida Statute §117.265. This recording, combined with the tamper-evident digital seal applied to the document, creates an audit trail that is far more robust than a traditional paper notary journal.

In the event of a dispute, a title company or lender can produce not just a record of the notarization, but a video of the entire signing — the signer's face, their ID, their verbal acknowledgment of each document. This is a level of evidentiary protection that paper-based closings simply cannot match.

III. The Loan Signing Deep Dive: Why "Any" Notary Won't Do

The notary industry has a well-documented quality problem. The proliferation of signing service platforms has made it easy for any commissioned notary to accept loan signing orders, regardless of their training or experience with real estate documents. The result is a re-draw rate that title companies and lenders absorb quietly — until it becomes a funding delay.

### The Certified Loan Signing Agent Difference

A Certified Loan Signing Agent (LSA) has completed specialized training beyond the state notary commission. This training covers the full anatomy of a loan package: the Promissory Note, the Deed of Trust or Mortgage, the Closing Disclosure, the Right of Rescission, and the dozens of lender-specific addenda that vary by transaction type and investor.

The difference is not academic. A trained LSA knows that the Closing Disclosure requires the borrower's signature on every page, that the Right of Rescission must be signed and dated correctly for the rescission period to be valid, and that a missing initial on the Note is not a minor clerical error — it is a reason for the lender to reject the package.

### The Hybrid Closing: The Industry Sweet Spot

The "Hybrid" closing model has emerged as the current industry standard for balancing efficiency with compliance. In a hybrid closing, the bulk of the loan package — disclosures, applications, and non-notarized documents — is executed electronically via e-signature platforms like DocuSign or Blend. The documents requiring notarization (typically the Deed of Trust and any affidavits) are then completed via RON with a certified signing agent.

This model delivers the best of both worlds: the speed and convenience of e-signatures for the majority of the package, and the legal robustness of a live notarization for the documents that require it.

### Error Prevention: The RON Advantage

Digital RON platforms include built-in compliance checks that prevent the most common signing errors. Before the session ends, the platform flags any unsigned or uninitiated fields, preventing the package from being submitted incomplete. This feature alone eliminates the primary cause of funding delays — missed signatures — that plague traditional in-person signings.

IV. The International Edge: Apostille Services in a Global Real Estate Market

For most domestic real estate deals, a notary seal is the final step. However, when the transaction crosses international borders, that seal needs its own "passport." This is where the Apostille comes in.

An Apostille is a specialized certificate issued by the Secretary of State that authenticates your notary seal for use in another country. It is recognized by the 129 countries that are members of the 1961 Hague Convention — a number that has grown significantly, with recent additions including Vietnam and Algeria.

### Common Real Estate Scenarios for Apostilles

The Expat Seller: A U.S. citizen living in Spain needs to sell their Florida property. They can use RON to sign the deed electronically, but Spanish authorities may require an Apostille on the notarized document to prove its validity.

The Foreign Investor: A developer from Brazil (a Hague member) is purchasing commercial property in the U.S. and needs to authorize a local representative via a Power of Attorney (POA).

Inheritance & Probate: When a property owner passes away, heirship affidavits or death certificates often require Apostilles to settle estates involving international assets.

### The Power of E-Apostilles in 2026

We are officially in the era of the e-APP (Electronic Apostille Programme). Because RON generates a digital original, this document can be submitted electronically to the state for an e-Apostille in many jurisdictions. What used to take two to three weeks of mailing paper can now often be completed in 24–48 hours — making a RON-capable notary an invaluable asset to any Realtor whose international client's closing is on the line.

V. Benefits for the Power Partners: Realtors & Title

### For Realtors: Close from Anywhere

The most common reason a real estate transaction falls apart at the closing table is not financing — it is scheduling. A client who is traveling for work, relocating from out of state, or simply cannot take time off during business hours represents a lost commission under the traditional model.

RON eliminates this constraint entirely. Your client can close from a hotel room in Tokyo, a vacation rental in Aspen, or their home office in Miami. The closing happens on their schedule, not the notary's.

### For Title Officers: Funding on Time

A perfectly executed digital package means no re-signs, no courier delays, and no last-minute scrambles to get a corrected document back to the lender before the rate lock expires. The RON platform's built-in compliance checks ensure the package is complete before it leaves the signing session. The tamper-evident seal ensures it arrives at the lender exactly as it was signed.

### For Homeowners: Convenience & Privacy

No strangers in the house. No scheduling conflicts. No driving to a title company office during a workday. The borrower signs from wherever they are most comfortable, in a session that typically takes 30–45 minutes from start to finish.

VI. Security & Compliance

### Tamper-Evident Technology

The digital seal applied by a Florida RON notary is cryptographically linked to the document's content at the moment of signing. If any character in the document is altered after the seal is applied — even a single comma — the seal visually "breaks" and the document is flagged as modified. This provides a level of document integrity that a wet-ink signature simply cannot match.

### MISMO Compliance

The Mortgage Industry Standards Maintenance Organization (MISMO) has established technical standards for electronic mortgage documents. RON platforms that meet MISMO standards ensure that the digital documents they produce are compatible with the systems used by lenders, servicers, and the GSEs (Fannie Mae, Freddie Mac). At Notary Catalyst, we use MISMO-compliant platforms exclusively.

### Data Privacy

All client PII (Personally Identifiable Information) collected during the RON session — ID images, KBA responses, and session recordings — is stored in encrypted form and is never shared with third parties. Our data retention and privacy practices comply with Florida law and are detailed in our Privacy Policy at notarycatalyst.com/privacy.

VII. Checklist: How to Prepare for Your First RON Closing

Hardware: A laptop, tablet, or smartphone with a working camera and microphone. A standard home WiFi connection is sufficient.

Identity: A valid, unexpired U.S. Driver's License, State ID, or Passport. A U.S. Social Security Number is required to pass the KBA quiz.

Documents: Your document in PDF format, uploaded before the session begins. If you only have a paper copy, photograph it and convert to PDF using any free app.

Environment: A quiet, well-lit room where you are the only person present (unless witnesses are required). The session is recorded, so a professional setting is recommended.

VIII. Conclusion: The Future Is Here

Digital closings are not a backup plan for when in-person signings are inconvenient. They are the preferred method for the modern consumer, the competitive advantage for the forward-thinking Realtor, and the operational upgrade that title companies have been waiting for.

Choosing a tech-forward, multi-certified notary is not just a convenience — it is an investment in a smooth closing, a funded loan, and a satisfied client who refers their friends.

Ready to streamline your next closing? Book a consultation at notarycatalyst.com or call (407) 891-4398. Our AI receptionist is available 24/7.